Medicare Supplement Plan Distribution Trends

Telos Actuarial publishes 16th Annual Market Projection.

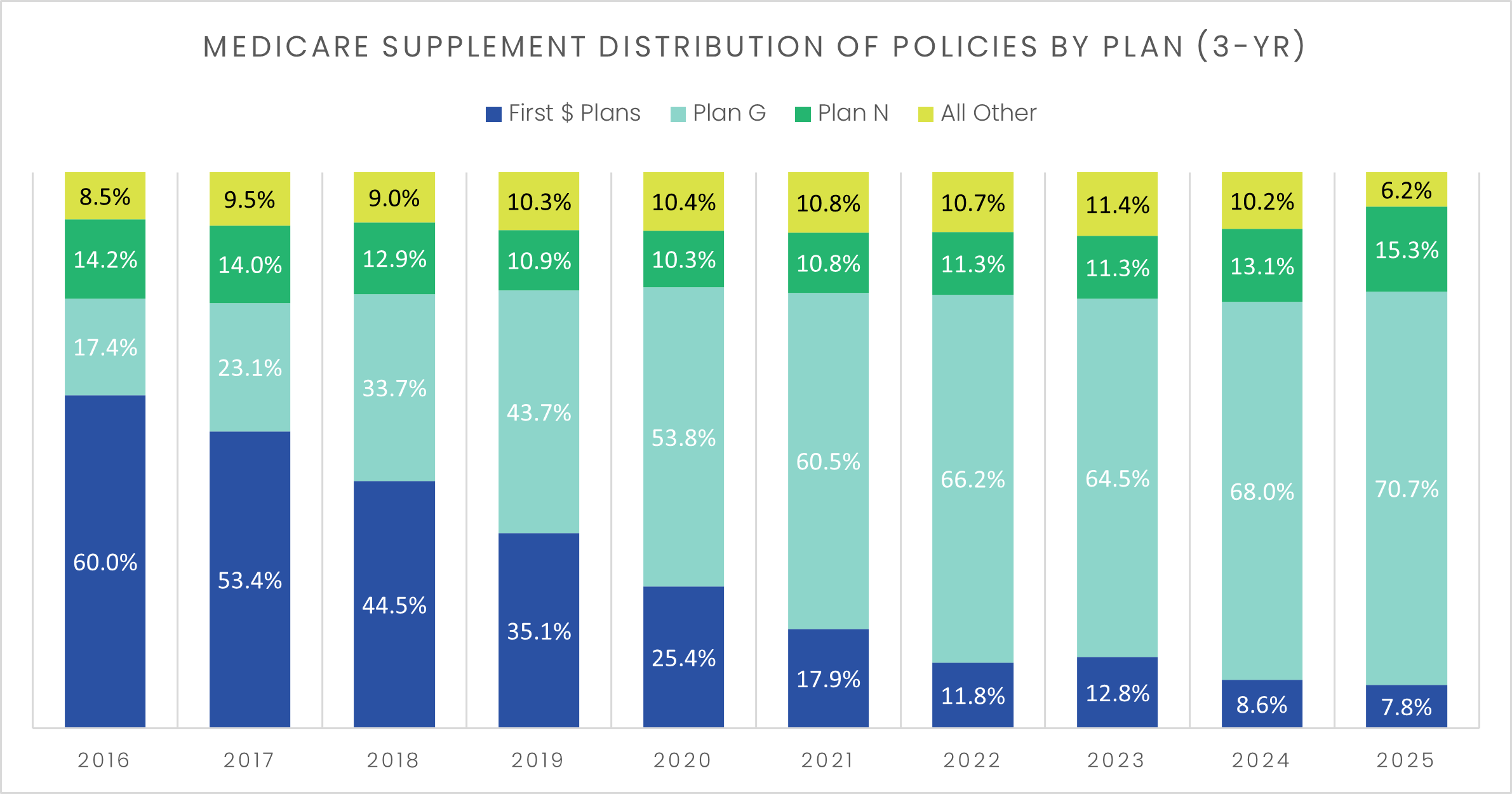

The Medicare supplement landscape has undergone a dramatic transformation over the past decade. The 2025 data illustrates that the era of first dollar coverage is firmly in the rearview mirror and that Plan N has been gaining some steam.

Beginning around 2013, Plan G gained serious traction as carriers started pricing it aggressively relative to Plan F. Even though the only meaningful benefit difference between the two plans was Plan F's coverage of the Part B deductible (just $147 in 2013), carriers were able to price Plan G at a discount that far exceeded that deductible amount. This made Plan G the economically rational choice for new enrollees willing to have some skin in the game. That shift accelerated dramatically following the passage of MACRA (Medicare Access and CHIP Reauthorization Act of 2015), which removed carrier’s ability to sell first dollar coverage plans, including Plan F, to individuals newly eligible for Medicare on or after January 1, 2020. MACRA also designated Plan G as the new guaranteed issue standard plan for newly eligible beneficiaries, effectively passing the torch from Plan F to Plan G as the market's flagship product.

The numbers tell the story. Looking at the distribution of lives (for policies issued within 3 years of the data reporting year), Plan G has grown from just 17.4% of lives in 2016 to 70.7% in 2025, while first dollar coverage plans have collapsed from 60.0% to 7.8% over the same period. The following graph highlights this dramatic shift:

While Plan G's dominance has been the headline story for years, 2025 introduces a new subplot worth watching: Plan N is quietly picking up momentum.

As shown above, in the new-issue market, Plan N lives jumped from 13.1% in 2024 to 15.3% in 2025 — its largest single year gain in the dataset. This signals that consumers and carriers alike are taking a fresh look at this lower premium alternative. Plan N offers most of the same coverage as Plan G but requires cost sharing at the point of service, along with exposure to Part B excess charges. In exchange, Plan N carries a noticeably lower premium than Plan G, which would tend to resonate with healthier Medicare beneficiaries who are willing to accept some additional out-of-pocket cost exposure.

For additional insights and analyses, download Telos Actuarial’s 16th Annual Market Projection here today!

The Telos Actuarial team boasts over a century of Medicare supplement experience. No matter where your company finds itself within the Medicare supplement product journey, we can help.

Contact us to find out more - info@telosactuarial.com!